"I tHoUgHt ThAt ToO tHiRtY yEaRs AgO yEt HeRe I aM"

Ok grandpa what was the debt-GDP then vs now

Ponzis are great until theyre not

So why do I have to keep paying social security taxes if it won't be there for me in 30 years?

Its a grift dude.

The premise of altruism is based on free choice.

If you did a pre tax contribution, you get to buy the full $10,000 worth of bitcoin instead of $8,500.

For 10 years of stacking, you now get 0.41 bitcoin and avoided $15,000 in tax. At year 10, your stack is worth $540,000. If you decided to take this as income as a lump sum, your average tax rate might be 26%, so don’t do that, you’d spend $140,000 in tax.

Instead, you work another 10 years but just stop contributing and spend the money you would have contributed instead. At year 20, your stack is worth $3,600,000.

At a monthly draw down of $14,500 and assuming this increases at 3% per year, you take out $175,000 a year (at the beginning and the inflation adjusted equivalent after that) and pay a tax of say $25,000-$35,000/ yr.

Let’s say you draw down at the same $14,500 per month. You money lasts at least until year 65. If you want to die at year 65 from now with nothing left, you can spend $15,250 a month.

So the Roth wasn’t the better deal here. I thought it would have been the opposite. I guess it would have been a better deal if bitcoin price didn’t rise so rapidly during the stacking period (pretax stack is considerably larger than the post tax Roth stack).

Note, future bitcoin prices above are estimated using power law model, which fits historical bitcoin price data far better than other models and produces reasonable future price predictions over several decades.

Main take away from this long analysis, for which I used a very complicated spreadsheet I’ve been working on for over a year, can be summed up by the freely given wisdom of nostr:npub1rtlqca8r6auyaw5n5h3l5422dm4sry5dzfee4696fqe8s6qgudks7djtfs : nobody goes in hard enough the first time. If I re-ran these scenarios starting 5 years ago, one could contribute just for the first year and still end up ahead of the 10 year stacker today. That said, stacking moderately for 10 years beats slaving away for 40 in the current fiat system.

It seems to me that self-custody bitcoin obsoletes Roths. Why put post-tax dollars in any investment vehicle other than self-custody bitcoin?

To my 83yo friend, it seems insane to not be maxxing IRA contributions. 15 years ago this wouldve been great advice.

To me, it seems insane to put in a trad IRA any more than the minimum to get an employer's matching contribution.

"Your post is very unpleasant to read for many and contributes to a hostile work environment." 😂😂😂

I thought Roths were funded with post-tax earnings?

So isn't that like buying self-custody bitcoin but with extra steps and kyc?

I think I may be misunderstanding why anyone would do this

I would jump at an 8-month severance buyout. Zero hesitation.

It'd be the Summer of Nate lol

Your family, health, & time will always be worth more than money

I was talking to an 83yo the other day.

He asked, "You are maxxing out your IRA contributions every year right?"

😂😂

Rumor has it Chuck's still napping after this heavy exertion

Its all fun and games until they require depositors to doxx their full utxo history before they can withdraw

You can see

On the public ledger

All by yourself

And you choose not to

Because ... ?

You're lazy?

They care more about winning than serving or solving problems.

CORRUPT

I always immediately believe the exact opposite of whatever Bill Gates says

Just sharing with you that you can look on-chain for yourself to see those addresses' activity.

Not attacking you king

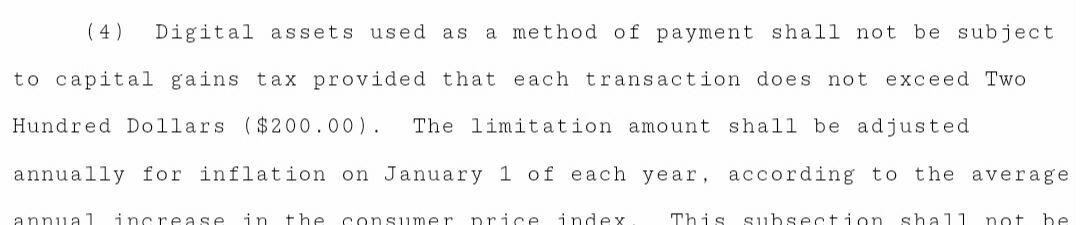

Its a particular state's proposal. If passed will take effect in that state July 1st.

Idk how they plan to enforce it for non-KYC sats on small things.

State-level #bitcoin fuckery.

Cap gains tax on any tx over $200 gtfo