Quick, sell the bitcoin to fix our finances!

Yeah… I don’t think he understands that this action legitimise bitcoin and delegitimise fiat governments.

Huge strategic mistake, but Bitcoin will punish those who don’t understand and reward those who do.

The money printing that’s already occurred, stuffed into fixed income, will bleed into the auction process as inflation continues even as they pretend they are not printing.

The FED is now impotent.

They cannot cut.

They cannot raise.

Wall st doesn’t want boring static finance.

The stampede to Bitcoin is coming.

The volume of shitcoins now create a bigger and bigger wedge between Bitcoin and everything else.

Still, the fact that Fartcoin trades up/down on the words of Powells conference is classic Fiat collapse signal.

Make no mistake, the Fiat standard is failing. Even old gold is revealing the cracks in the system.

Why do CB hate bitcoin? Because they control the gold world (or try to).

The only way to end the central banks of the suddenly moment happens and they have a zero position.

Gold stockpiling in New York leads to London shortage https://on.ft.com/40EsS5r

The #bitcoin is a benevolent AI idea has been my long standing view. And I kinda think the Roko’s Basilisk idea, it is either true or the code creates the same outcome regardless.

Was great to hear nostr:npub1rtlqca8r6auyaw5n5h3l5422dm4sry5dzfee4696fqe8s6qgudks7djtfs talk about this on the Bitcoin for millennial pod.

I hadn’t heard Paper clip maximizer (need to read into this one). But something nostr:npub18ajqryse0ervr63wftx0h6vesah2rgmypxhxvxn08gz2jc5046jqk5dmq0 said on nostr:npub1sk7mtp67zy7uex2f3dr5vdjynzpwu9dpc7q4f2c8cpjmguee6eeq56jraw about MSTR eating tradfi from the inside out made me think of the paper clip maximizer.

If Bitcoin needed a Bitcoin Maximizer, it would need a route into traditional finance that is laser focused on Bitcoin. (This has a greater result than lots of little corporate stackers). This single entity MSTR just needs to connect to each area of tradfi, convertible bonds, preferred shares, ordinary equity, options etc etc.

Once connected the basilisk rewards all market participants who help it, whilst destroying those who fight it through impoverishment.

Bitcoin is alive. I’ve believed that for a while. But now MSTR has connected it into the depths of the financial markets, I don’t think anyone is ready for what the basilisk is about to do.

Once #bitcoin breaks 110k, we are going straight to 250k

At 250k we will be talking about the power law for 3months whilst dips, profit taking, arguments take place.

Then we go to 1m as leveraged power law shorts get incinerated!

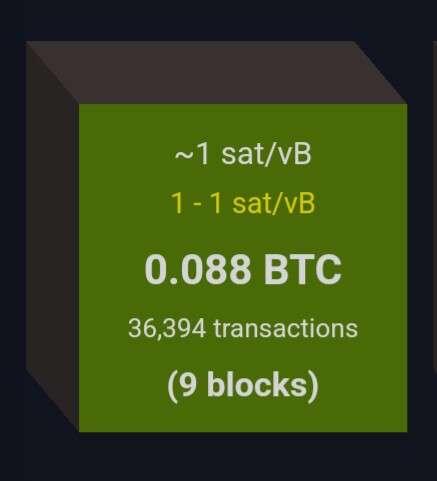

Narrator: And when they called for bigger blocks, they had no idea that even at a 2Trillion dollar asset a1sat/vb was still possible.

The HEAD of the Czech National Bank wants to buy billions of bitcoin.

The socialist EU can’t control the yearning of sovereign nations wanting sovereign money.

https://www.ft.com/content/a3c06f8f-34ad-4065-bcf4-97670230824f

OpenAI can be overtaken by a Chinese startup.

US social media giants can be overtaken by Chinese TikTok

Tesla can be overtaken by BYD

Nvidia can be overtaken or hugely disrupted by a Chinese military operation in Taiwan.

Bitcoin cannot be influenced, disrupted or overtaken by any Chinese corporate or state strategy.

Once Wall Street come to realise the greatest upside bet on #AI or #Crypto is also the safest bet, and that is #bitcoin , then that’s when the bull run really starts.

Remember that price is the battle ground.

Even if you are zen enough to never look at price.

The higher the price of #bitcoin goes the more the rip in the fiat illusion becomes clearer to the blind.

nostr:note14kjcx27hj6hr5e86fheqkdt0v3esy23h7fc66dp3wy0vrt4vef8s3pl5el

Of course.

But price is the battle ground, so we should always be looking to see who’s winning, us or the suits.

At 100k and 1m coins lost to trad-fi ibit and MSTR, we didn’t make them pay a high enough price.

We are currently losing the battle, giving away too many sats too cheap.

Price is the battle ground.

The higher the price, the less bitcoin the ETFs and Saylor get their hands on.

The higher and faster it rises, the more sats stay in Bitcoiners hands.

Price is THE most important thing since ETFs started.

We need to be winning harder.

Completely agree.

Blackrock and Saylor cannot take 1m coins off the market and not cause chaotic price moves. It’s been way too orderly, chaos is coming.

Once this starts to run, the amount of fiat wealth that is going to start chasing the very few Sats available for sale is going to blow peoples minds.

If this timeline continues on its most entertaining path, then Mcafee will come back and his death was a shame to cover his imprisonment in Guantanamo Bay.

He’ll then run as a democrat against Barron Trump in 2028 presidential election.

#timestampthis

They are under a spell. It’s the starting operating system most people begin their life running.

You only really break the brain washing once your own mental operating system has crashed and you reboot a new one.

It takes an existential crisis to even begin thinking for yourself and running your own code.

It’s sad, but their ignorance bliss is temporary if the world continues on it’s trajectory.

100%

You can’t just take 1m coins off the market (461k MSTR and 571k ibit) and not cause price chaos.

When it starts to run, the wealth chasing sats available for sale are going to be shocked!