EVERY BLUE CHECK THAT KNOWS ABOUT NOSTR BUT CHOOSES NOT TO USE IT IS SHORT BITCOIN.

NO ZAPS FOR THEM.

What is a blue check? Is it on Damus or Primal?

How do you orange pill by proxy?

And besides, I have started to get the massages from normal people on how to buy now. I keep calm, and send them to Bare Bitcoin, K33 and kryptopris dot no. But inside my own head I am screaming: «why didn’t you listen 1,2,3 years ago?»😂

Looking great! PoW💪 Ordered the book, and payed with bitcoin, of course. Use sound money to buy value! nostr:note1chq5v2p9e8qvq5ls8hzvqagpfyaql0gdd25nv6e9ax9j60ad7l7qqp7n9j

Winter is coming🪵🪓🔥

#proofofwork #norgstr #noregstr

En del bra på Trygdekontoret. Bare synd de fleste episodene er «NRK app only». Jeg boikotter de når jeg ikke får velge avspiller selv (Fountain)

GM🫖🍵

Finally managed to orange-pill my brother-in-law this weekend while we were staying over for my son’s football tournament.

I’ve been dropping hints to him about Bitcoin for a couple of years—small nudges, sharing an article here and there. He’s always been interested in stocks and economics, listens to podcasts, but I could never quite get him to fully consider Bitcoin.

I recently sent him Seetee’s Letter to Shareholders and the Bitcoin Whitepaper. The shareholder letter actually sparked his interest. Later, as he helped me cut down seven trees this fall, we talked a lot about Bitcoin, and I could tell his curiosity was growing.

I also sent him a podcast episode on Austrian economics from @Andreas Harding, featuring Ole Emil Augland and Hjalmar Hauge, and that really caught his attention.

But then, he sent me a few podcast recommendations on gold and silver, mentioning he was considering buying shares in MicroStrategy or investing in gold and silver.

That’s when I decided to go all in. I explained that, yes, MicroStrategy does have exposure to Bitcoin’s price with leverage—and all the tricks that come with fiat. He responded, “You Are right, you never know what the company might decide to do in the future.”

Then I showed him the @fountain_app, where you can support with sats by “boosting.” I used @RabbitHoleRecap and the split between @ODELL and @MartyBent as examples. That’s when things clicked for him—the idea that you can send just 10 sats per minute ($0.007), something impossible with fiat because of transaction costs.

Since he works in imports, he understood this right away. I went on to explain that traditional economics often misses the fundamentals, saying things like, “There’s no revenue in Bitcoin, so the value must be zero.” But if the entire world used Bitcoin, global GDP could grow by 2-3% purely from transaction cost savings. He even pointed out that we wouldn’t need every company or customer on board—a small percentage adopting Bitcoin could be enough to push fiat to become cheaper and more efficient. But fiat just can’t compete with that. So then…

He’s still eager to read, listen, and learn a bit more before committing larger amounts, but I just got a screenshot: he’s bought his first sats through Bare Bitcoin and is setting up a small DCA plan with each paycheck.

The perfect start to a Sunday.

Only way this day could get better is with good results at my son’s football tournament and a Tottenham victory over Palace this afternoon! 😁

Here he is, helping me with those big trees. Now I’ve returned the favor by helping him start down the rabbit hole. PoW💪  https://video.nostr.build/d96ced7b6df51e43f250bef84e0b97c35dc65fde9da40cee31f53186dc88c211.mp4

https://video.nostr.build/d96ced7b6df51e43f250bef84e0b97c35dc65fde9da40cee31f53186dc88c211.mp4

Klar for «Hva skjer med krona?» på Kåkånomics i Stavanger.

Heldigvis har vi bitcoin😁

They can still blame it on the safety of the driver. The box could be a honeypot for robbers.

The bus companies get away with this argument, so they are exempted from taking cash.

That is, they have to accept other means of payment than an app. For instance, in rural areas with 2-3 buses a day and a large elderly population that need the bus to get to the hospital (which is centralized to the city an hour or two away to save money), you can send in payment via bank (or maybe cash?) and get the ticket in the mail (which is only delivered every other day except weekends, again too save money).

So the focus of a cashless society in Norway is less about privacy and more about those who struggle with apps.

They won’t take cash on the bus. They blame it to the safety of the drivers. Risk of beeing robbed. In reality it’s because it is a hassle for them. Takes time for the driver to accept cash

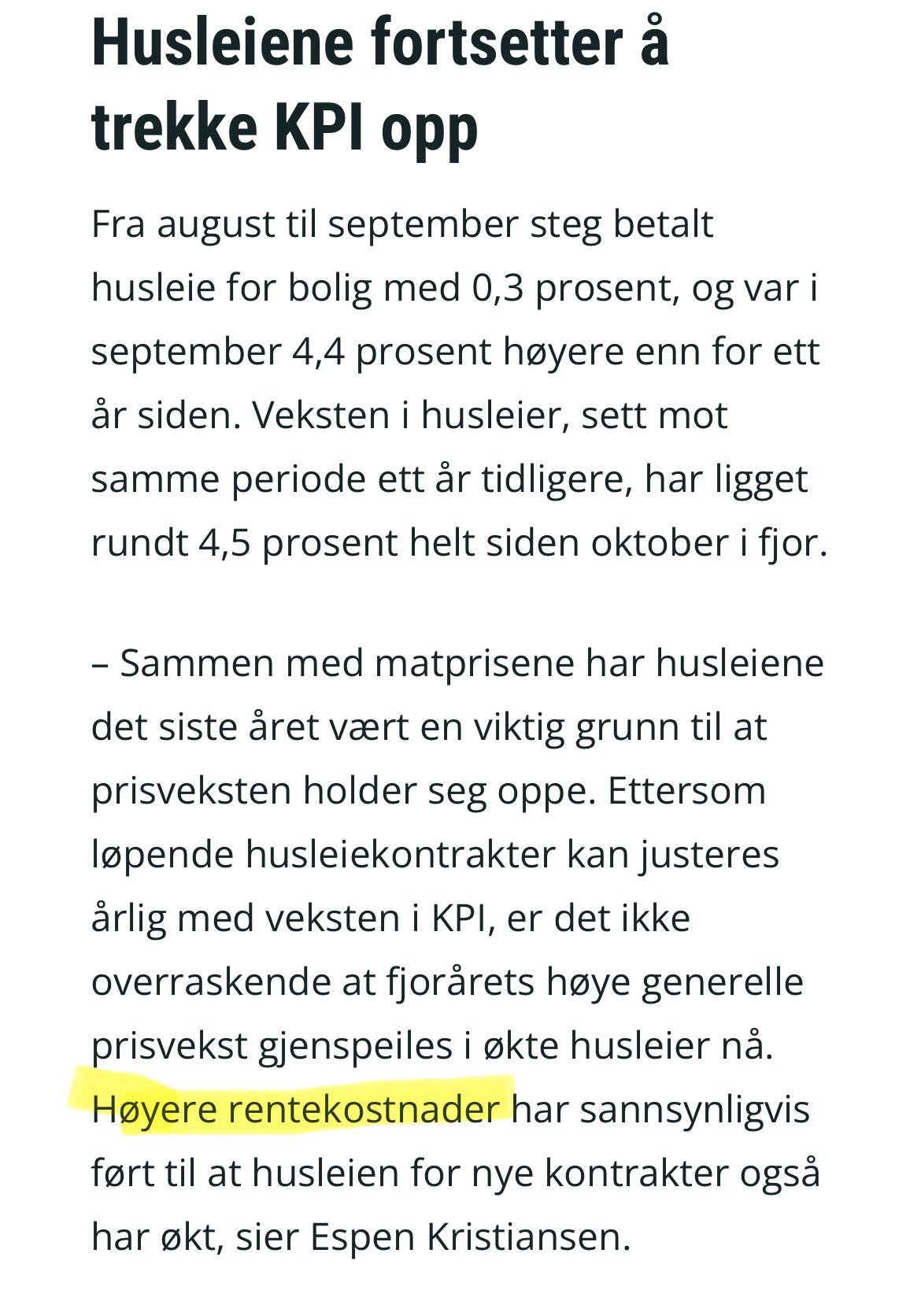

The Circle of CPI:

In Norway, interest rates are still being kept high by the central bank because inflation is high.

According to Statistics Norway (SSB), inflation is high because high interest rates lead to high housing rental costs.

A productive weekend. PoW. nostr:npub1xcrkgfqejzgqaxle4jhmuyp8g0xpjvsug4yt6ayxw8r7p02j3gjscl60yf, take a bow😁 #noregstr #norgstr https://video.nostr.build/e0147724d1de981a1cf11f6f17520775a13c14668769b943818eb70a3b311d63.mp4 https://video.nostr.build/61275b6ea2188b3984b3d578d4ed4838f1635082388d2e575263a418ae4f4e2b.mp4  https://video.nostr.build/dddcc00f80016ff85aaa79f3a107136a85d78ad91bce15198f15eef630e6ddc1.mp4 https://video.nostr.build/da1fb302f072939b26f7076aeff5df9254399418fef3d4d8d002eece3b9cc717.mp4

https://video.nostr.build/dddcc00f80016ff85aaa79f3a107136a85d78ad91bce15198f15eef630e6ddc1.mp4 https://video.nostr.build/da1fb302f072939b26f7076aeff5df9254399418fef3d4d8d002eece3b9cc717.mp4

Simualar to «rammelån» / «flexible credit». See my full note in another reply to your post.

Traditional mortgages in Norway do not work the same way as in the US or UK. We don’t compound the interest on a mortgage.

In that regard, there is less difference between a normal mortgage and a HELOC (“flexible credit”) in Norway.

Norway: Interest is calculated on the principal during each payment period without being added to interest from previous periods. This means that you don’t pay interest on interest, unlike with compounded interest.

USA/England: Interest accrues over time and can “compound,” creating a snowball effect because you pay interest on previously accumulated interest.

This means that mortgages in Norway can be more favorable in terms of interest over time, as you only pay interest on the remaining principal, not on previously accrued interest.